All About Residential Land Supply

As at 2021 Q1

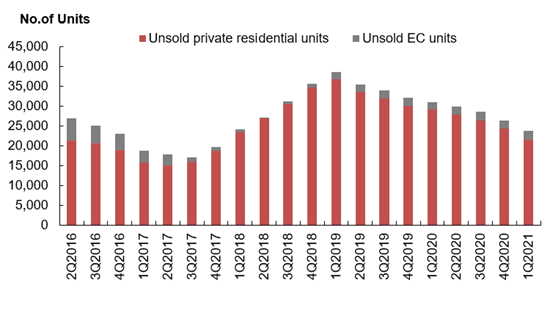

Total number of unsold private residential units in the pipeline

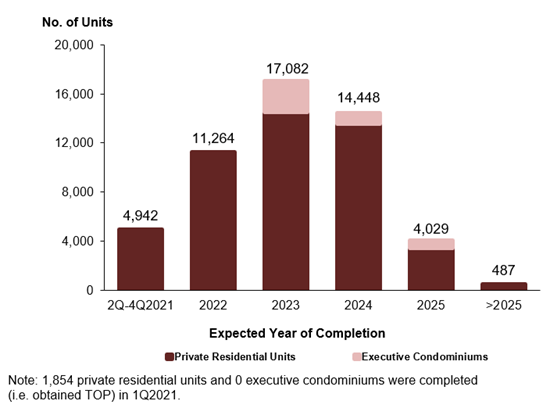

Based on the expected completion dates reported by developers, 4,942 units (including ECs) are expected to be completed in the remaining 3 quarters of 2021. Another 11,264 units (including ECs) are expected to be completed in 2022.

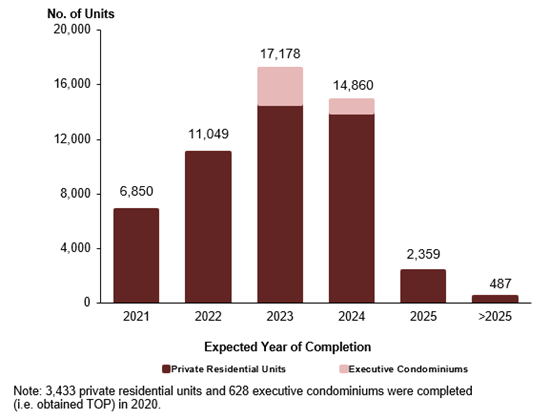

Pipeline supply of private residential units and ECs (with planning approvals) by expected year of completion

Apart from the 23,735 unsold units (including ECs) with planning approval as at the end of 1st Quarter 2021, there is a potential supply of around 3,840 units (including ECs) from Government Land Sales (GLS) sites that have not been granted planning approval yet.5

The supply of private housing in the pipeline, including from GLS sites, will sufficiently cater to the housing needs of the population when completed over the next few years. The Government will continue to monitor economic and property market conditions closely and adjust the supply of future GLS Programmes, where necessary, to ensure it remains adequate in meeting demand.

Stock and Vacancy

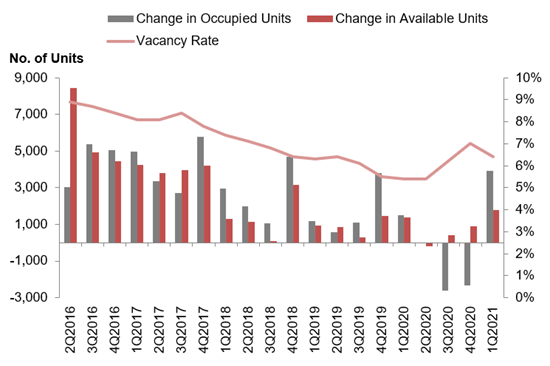

The stock of completed private residential units (excluding ECs) increased by 1,777 units in 1st Quarter 2021, compared with the increase of 884 units in the previous quarter. The stock of occupied private residential units (excluding ECs) increased by 3,942 units in 1st Quarter 2021, compared with the decrease of 2,339 units in the previous quarter. As a result, the vacancy rate of completed private residential units (excluding ECs) decreased to 6.4% as at the end of 1st Quarter 2021, from 7.0% in the previous quarter

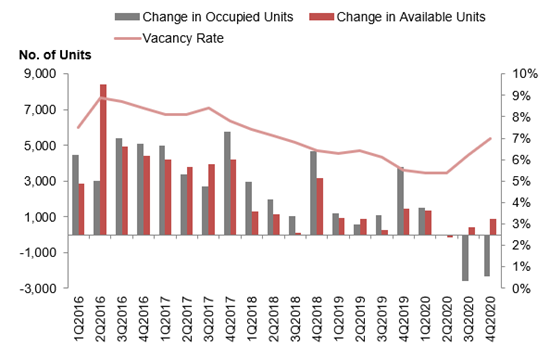

Stock and vacancy of private residential units (excluding ECs)

Vacancy rates of completed private residential properties as at the end of 1st Quarter 2021 in CCR, RCR and OCR were 9.5%, 6.1% and 5.3% respectively, compared with the 11.0%, 7.3% and 5.1% in the previous quarter

ReferenceAs at 2020 Q4

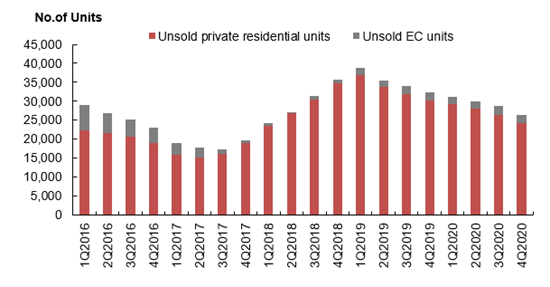

Total number of unsold private residential units in the pipeline

Based on the expected completion dates reported by developers, 6,850 units (including ECs) will be completed in 2021. Another 11,049 units (including ECs) will be completed in 2022.

Pipeline supply of private residential units and ECs (with planning approvals) by expected year of completion

Apart from the 26,426 unsold units (including ECs) with planning approval as at the end of 4th Quarter 2020, there is a potential supply of around 4,700 units (including ECs) from Government Land Sales (GLS) sites that have not been granted planning approval yet.5

The supply of private housing in the pipeline, including from GLS sites, will sufficiently cater to the housing needs of the population when completed over the next few years. The Government will continue to monitor economic and property market conditions closely and adjust the supply of future GLS Programmes, where necessary, to ensure it remains adequate in meeting demand.

Stock and Vacancy

The stock of completed private residential units (excluding ECs) increased by 884 units in 4th Quarter 2020, compared with the increase of 404 units in the previous quarter. The stock of occupied private residential units (excluding ECs) decreased by 2,339 units in 4th Quarter 2020, compared with the decrease of 2,605 units in the previous quarter. As a result, the vacancy rate of completed private residential units (excluding ECs) increased to 7.0% as at the end of 4th Quarter 2020, from 6.2% in the previous quarter

Stock and vacancy of private residential units (excluding ECs)

Vacancy rates of completed private residential properties as at the end of 4th Quarter 2020 in CCR, RCR and OCR were 11.0%, 7.3% and 5.1% respectively, compared with the 9.2%, 7.4% and 4.2% in the previous quarter.

Reference